Scrip’s Rough Guide On The State Of RNAi

How Will RNA Modalities Stack Up Against Gene Therapy?

Executive Summary

The introduction of gene therapies has been the highest-profile new modality to reach the market, but new RNA-based therapeutics hold significant potential and could be more accessible for patients. Scrip reviews the leading drug developers in this space.

Much of industry's current attention is focused on gene therapies – and rightfully so, considering the therapeutic promise of such one-time cures, and the spate of M&A activity for gene therapy biotechs and manufacturers, despite justifiable concerns over its scalability and affordability. But some of those challenges serve to highlight the opportunities possible with a different breakthrough field – drugs that target RNA, either through double-stranded RNA-mediated interference (RNAi) or antisense oligonucleotides (ASOs).

Arguably overshadowed by gene therapies and their curative hype, RNA therapeutics are gaining prominence, with a number of approvals in rare disease settings and potential applications in highly prevalent indications. As the technology has been honed over the past decade, the latest generation of RNA-targeting drugs is seamlessly progressing through clinical development with a high probability of success.

Being just one step removed from the underlying genetic mutations, targeting RNA offers a closely related treatment modality to gene therapy with greater control over dosing and potential side effects. Although lacking the duration of effect, administration as infrequently as every six to 12 months may be a blessing in disguise and avoid complex payment systems that threaten to hinder market access for gene therapies.

Intensifying Competition Between Two Emerging Drug Platforms

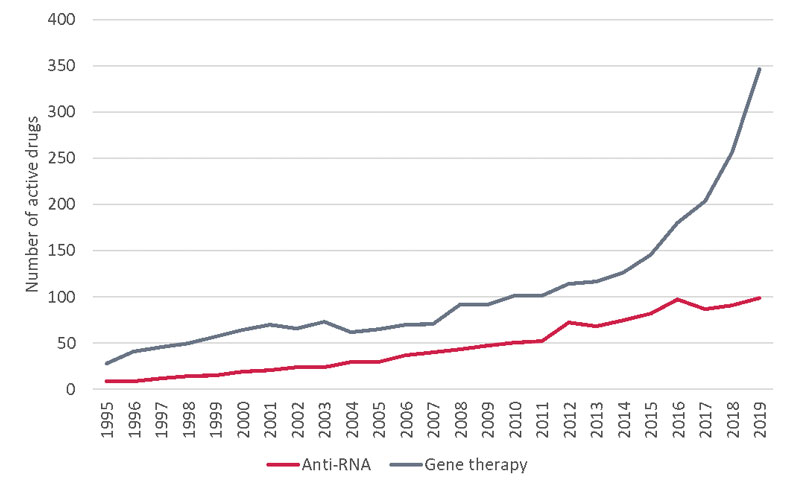

The pipeline for RNA-targeting drugs is certainly busy, now exceeding 100 clinical-stage candidates for the first time, and thus far has yielded nine approved therapies. R&D database Pharmaprojects is tracking a further 200 preclinical-stage projects, pointing towards a healthy appetite for further investment in this emerging drug platform. The comparison between pipelines of RNA-targeting drugs and gene therapies does favor the latter, especially in the last few years (see below), but the work of pioneering companies in this field such as Ionis Pharmaceuticals Inc. and Alnylam Pharmaceuticals Inc. should not be discounted.

As the science is further validated across new therapy areas, and reaches commercial milestones, we can certainly expect these companies to increasingly enter the crosshairs of big pharma. Novartis AG’s takeout of early RNAi developer The Medicines Co. in late 2019 for $9.7bn sets an impressive benchmark for potential valuations, and may spur on its competitors to also act quickly. (Also see "Novartis To Pay $9.7bn For The Medicines Company" - Scrip, 24 Nov, 2019.)

As with gene therapy valuations, much of the value is derived not only from the clinical-stage assets themselves, but also the technological capabilities. RNA-targeting discovery platforms offer the ability to manipulate genetically validated targets with high selectivity and infrequent dosing, in particular targeting “gain of function” mutations that increase aberrant protein production and are not directly addressable via gene therapy.

The Growth Of RNA And Gene Therapy Assets

Pharmaprojects

Pharmaprojects

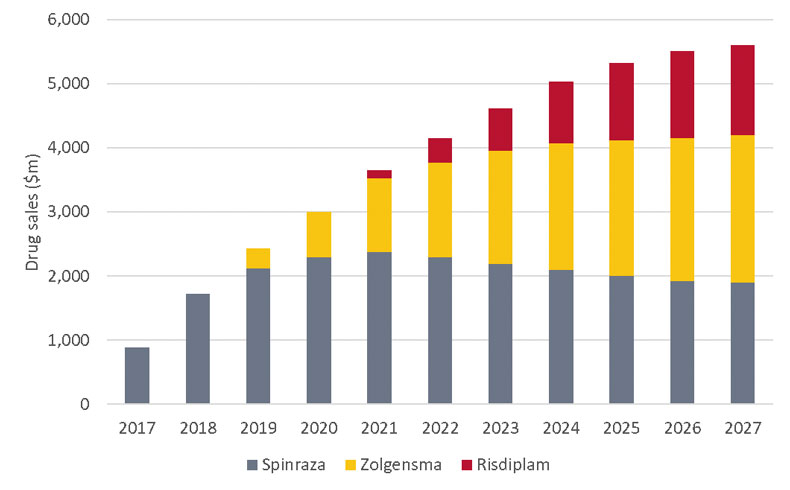

Although both technologies have only relatively recently entered clinical practice, the first battleground is already set – spinal muscular atrophy (SMA). Patients with SMA carry mutations in the SMN1 gene, resulting in a lack of SMN protein, which is essential for neuronal growth. In 2016, Biogen Inc. gained approval for Spinraza, an RNAi therapy that binds a non-coding region of SMN2 mRNA and encourages splicing, increasing the production of functional SMN protein. SMN2 is a homologous gene for SMN1 and under normal conditions only produces a minority of the total SMN. Spinraza has since established itself as a standard-of-care and is on course to notch over $2bn in 2019 sales, although it did record a slight dip in the quarter that Zolgensma, a rival gene therapy marketed by Novartis, launched. (Also see "Novartis's Zolgensma Finds Commercial Legs In A First For Gene Therapy" - Scrip, 22 Oct, 2019.)

As a gene therapy, Zolgensma is able to directly address the underlying mutation in SMN1 that causes SMA, delivering a corrected version of the gene via an AAV vector. Despite fighting against a high-profile data-manipulation scandal, Zolgensma’s launch has exceeded analyst expectations and it may yet become the future SMA market leader, even factoring in competition from subsequent launches. Further development of the two products, including new formulations and expanded age groups, will determine the balance of power, but both products will be able to co-exist and remain lucrative. (Also see "The SMA Market: Assessing The Unknowns" - In Vivo, 26 Nov, 2019.)

Spinal Muscular Atrophy Market Forecast, 2017-27

Datamonitor Healthcare, Drug Sales Analytics

Datamonitor Healthcare, Drug Sales Analytics

Hemophilia may become the next tussle between the two, with Sanofi’s fitusiran acting to silence antithrombin – the final common pathway in the clotting cascade and amenable across all patient types – while a range of gene therapies are seeking to normalize endogenous factor VIII or IX levels in hemophilia A and B, respectively. (Also see "Momentum Builds For Tomorrow's More Convenient Hemophilia Drugs" - Scrip, 13 Jul, 2017.)

Beyond these examples, there is an ongoing tug of war between RNA technologies and gene therapies when it comes to deal-making and fundraising. Gene therapy is being backed with greater resources, as made evident by its comparably larger pipeline and clinical trial activity, not to mention the multiple blockbuster acquisitions by big pharma. Novartis is one notable company with fingers firmly in both pies, with its Medicines Co. acquisition coming shortly after a similar $8.7bn transaction with AveXis Inc. to gain access to Zolgensma.

Company By Company – A Review Of RNAi Leaders

Alnylam Sets Expansive Strategy And Reveals Aspirations In CNS And Ocular Diseases

Alnylam is on course to exceed the goals set in its 2020 vision, with the company expecting to operate in four strategic therapeutic areas with four different drugs by the end of the year, while building a pipeline of 14 clinical-stage drugs, of which six will be in late-stage development. The engine for this success has been its RNAi platform, now delivering between two to four IND-stage candidates each year. (Also see "Alnylam Interview: RNAi Leader Expands Into NASH, CNS And Eye Diseases" - Scrip, 8 Jan, 2020.)

With its first approved therapy Onpattro (patisiran), Alnylam is building a keystone franchise that it hopes to establish into a multi-billion-dollar anchor point, driving the company eventually into profitability and funding continued expansion. 2019 sales came in at $166m, so Alnylam will need significant progress with Onpattro’s target population to include all ATTR amyloidosis patients and scaling of commercial activities.

While its second approved drug, Givlaari (givosiran), has smaller commercial potential, it validates the strength of Alnylam’s discovery platform and has enabled the creation of a unique, prevalence-adjusted payment agreement. Royalty streams from collaborations with Novartis and Sanofi will provide the company with exposure to high-value growth markets in hypercholesterolemia and hemophilia while it commercializes its next late-stage orphan drugs, vutrisiran and lumasiran.

Lastly, Alnylam is attempting to develop its RNAi platform to address new targets outside of the liver, including central nervous system and ocular diseases. Its preliminary work in mice models suggests that an RNAi approach can knock down amyloid precursor protein, implicated across a number of neurological disorders, with a highly durable effect.

Ionis Continues To Accrue Development Partners And Progress Its Internal R&D Assets

Ionis is pursuing a slightly different business model to Alnylam, opting to out-license its leading assets to development and commercial partners while reinvesting into an extensive pipeline of its own. So far, this has yielded three approved antisense drugs, the most notable of which being Spinraza. This de-risked approach allows the company to be highly profitable, with Ionis reporting a record year for 2019: $1bn in revenues and $300m net profit, with a cash position of $2.2bn providing notable operational flexibility. As such, it relies heavily on partners to create and expand the markets for its ASO technology.

Although the next commercial launch is not expected until 2021 – the Biogen-partnered tofersen in development for amyotrophic lateral sclerosis (ALS) patients – 2020 will be a busy year in terms of pipeline advancement. This includes the continuation of four current Phase III programs, three new Phase III initiations, more than 10 new Phase II projects, and six new diseases with clinical proof of concept. Ionis has set the goal of achieving at least 10 NDA submissions by 2025, assigning a high probability of success for each of its pipeline projects owing to its antisense technology and genetically validated targets.

In addition to tofersen, the other notable partnered late-stage programs are TQJ230, partnered with Novartis for cardiovascular risk; RG6042, partnered with Roche for Huntington’s disease; and IONIS TTR-LRx from subsidiary Akcea Therapeutics Inc. for hATTR amyloidosis.

The focus of Ionis’ internal pipeline remains on high unmet need neurology indications, where its technology is being applied across a variety of rare indications, in addition to highly prevalent diseases such as Alzheimer’s and Parkinson’s. Outside of CNS, the broader Ionis-owned pipeline is looking at non-neurological rare diseases, in addition to cardiometabolic and renal, and cancer. Improvements in its drug discovery platform are also enabling new dosing routes, with a validated once-daily tablet being trialed for a cardiovascular indication. Ionis also hopes to achieve clinical validation for pulmonary and ocular delivery routes, which would allow for new opportunities in diseases such as IPF, PAH and retinal disorders.

Sarepta Advancing RNA Capabilities But Diversifying Towards Gene Therapies

Sarepta originally made a name for itself in the field of RNA therapeutics, designing ASOs that encourage exon skipping and production of functional dystrophin in Duchenne muscular dystrophy (DMD) patients. Its two approved drugs, Exondys 51 (eteplirsen) and Vyondys 53 (golodirsen), allow the company to target approximately 20% of DMD patients based on their genotype. However, it is now pivoting towards gene therapy and gene editing in the longer term.

Its most attractive candidate is SRP-9001, which delivers a truncated but functional version of the dystrophin gene and is amenable for all DMD patients. Data for the four patients dosed so far with nine months of follow-up have been impressive, showing functional improvement where the natural history is progressive decline, so it is logical that in this particular example Sarepta is favoring gene therapy for its longer-term ambitions. There are plans to aggressively pursue pivotal clinical development and achieve commercial-scale manufacturing, boosted by an ex-US partnership with Roche worth $1.15bn up front and $1.7bn in milestones. (Also see "Sarepta Secures $1.15bn From Roche In Ex-US DMD Gene Therapy Deal" - Scrip, 23 Dec, 2019.)

Nevertheless, Sarepta's pipeline of RNA programs now totals 14, growing from last year. One of these is casimersen, which extends an RNA therapeutic treatment option to DMD patients with mutations amenable to exon 45 skipping, which is a further 10% of the prevalent population. With a rolling NDA now submitted, this would become Sarepta’s third internally discovered drug to attain regulatory approval. (Also see "J.P. Morgan Notebook Day 1: No Big Deals, But Plenty Of Pipeline, Commercial Highlights" - Scrip, 14 Jan, 2020.) Its next-generation ASOs involve peptide conjugation and could lead to higher dosing and direct delivery to new muscle types, such as the heart.

Biogen’s Research Partnership With Ionis Is Bearing Further Fruits

While Biogen has a broad therapeutic focus, it owns the most commercially successful RNA therapeutic in Spinraza for SMA, with more than 10,000 patients on therapy and annualized sales of approximately $2bn. SMA will remain an important area of investment for Biogen in light of competitive threats, and lifecycle management of its Spinraza franchise is ongoing, with higher doses and novel ASO drug candidates under development.

Beyond its interests in SMA, Biogen reiterated at J.P. Morgan the timeline for its Phase III program of tofersen, an ASO-binding SOD1 licensed from Ionis for the treatment of ALS. The VALOR trial, recruiting 183 SOD1+ patients, is due to read out in 2021. Biogen also expects to provide a clinical update for its Phase I trial of its anti-C9orf72 ASO BIIB078, addressing the most common familial cause of ALS, on a similar timeframe. Biogen’s early development pipeline lists BIIB094, an ASO targeting genetic subsets of Parkinson’s disease, as well.

Novartis Paving The Way For Broad Adoption Of Inclisiran

Although Novartis hosted an investor call immediately following its announced acquisition of The Medicines Company and the RNAi asset inclisiran in November 2019, the company again took the opportunity to explain its rationale at the J.P. Morgan conference. With the deal now closed, Novartis becomes the only big pharma with presence across four advanced therapy platforms: cell, gene, radioligand and RNA therapies. This move to diversify and minimize reliance on single products and technologies is undoubtedly a driver behind the acquisition, but it also allows Novartis to operate within cardiovascular population health.

When critically appraising pipeline assets, Novartis CEO Vas Narasimhan said he poses three internal questions: “Are we really first in class, can we replace the standard of care, and do we have significant absolute efficacy gains in the medicines we launch?” Due diligence behind the Medicines Co deal will have given a resounding yes to each of these, in order for Novartis to part with $9.7bn.

A small-interfering RNA drug that offers twice-yearly option for inhibiting PCSK9, inclisiran was filed with the FDA for risk reduction in cardiovascular disease in December 2019, meaning Novartis is guiding for a 2020 approval, with submission to the EMA also expected in Q1 2020. Uniquely, Novartis is collaborating with the UK government prior to its approval, with a large-scale trial among NHS patients set to start later this year, ahead of a population-level agreement to ensure market access following approval. The UK government anticipates that the introduction of inclisiran on the NHS has the potential to save up to 30,000 lives over the next 10 years. (Also see "Novartis Inks World-First Pact With NHS England For Inclisiran" - Scrip, 13 Jan, 2020.)

Novartis also profiled a second antisense drug in its pipeline, TQJ230, which targets lipoprotein(a), one of the main genetic determinants of cardiovascular risk. Originally discovered by Ionis, the drug has demonstrated very potent reductions in this biomarker, leading Novartis to exercise an option to in-license the drug. The company confirmed its plans to initiate Phase III development during 2020, conducting a major outcomes study, although this was first announced back in February 2019.

Dicerna Starting A Big Year

Dicerna Pharmaceuticals Inc., headquartered in Lexington, MA, just down the turnpike from Alnylam in Cambridge, has spent years in the shadow of RNAi frontrunner Alnylam working through an intellectual property dispute. But a pair of recent deals is setting Dicerna up for a pivotal year.

In October, Dicerna signed a major deal with Roche to develop novel therapies for the treatment of chronic hepatitis B virus (HBV) infection, focused on its lead candidate DCR-HBVS, currently in Phase I.

The following month, it signed an agreement with Novo Nordisk AS to discover and develop novel therapies for the treatment of liver-related cardio-metabolic diseases, including chronic liver disease, non-alcoholic steatohepatitis (NASH), type 2 diabetes, obesity and rare diseases.

These plus an expanded collaboration with Alexion Pharmaceuticals Inc. and an existing partnership with Eli Lilly & Co., have given Dicerna more than $500m in upfront payments to help fuel its development pipeline, which will reach some crucial milestones in 2020. The firm remains in head-to-head competition with Alnylam, as Dicerna’s lead candidate (wholly owned) DCR-PHXC targets the ultra-rare kidney disease primary hyperoxaluria (PH) – where Alnylam has a commanding lead with lumisiran. (Also see "Dicerna Ready To Challenge Alnylam’s RNAi Dominance In 2020" - Scrip, 6 Jan, 2020.)

Arrowhead Getting Ahead By Partnering

Like Dicerna, Arrowhead Pharmaceuticals Inc. is moving to the next level via big pharma partnerships.

J&J’s Janssen Pharmaceutical Cos. unit placed a major bet on Arrowhead’s RNA-interference technology and subcutaneous delivery platform with a deal announced October 2018 to license ARO-HBV, Arrowhead’s gene-silencing candidate for hepatitis B, invest in Arrowhead and collaborate with the biotech on up to three additional novel targets. (Also see "J&J Bets Big On Arrowhead’s Early Promise In Hepatitis B" - Scrip, 4 Oct, 2018.) J&J has cited the deal as the beginning of a move to embrace RNA technologies. (Also see "Where Is J&J Investing For The Future? Cell Therapy, Gene Therapy And RNA" - Scrip, 16 May, 2019.)

When the J&J tie-up was announced in 2018, Arrowhead CEO Christopher Anzalone said the firm would focus on other programs centered around “validated targets, understandable regulatory pathways and clear commercial opportunities.” Since then, it has moved ARO-AAT into Phase II for liver disease associated with alpha-1 antitrypsin (AAT) deficiency and advanced a pair of lipid-lowering candidates, ARO-APO3 for hypertriglyceridemia and APO-ANG3 for dyslipidemia, into Phase I.

Arrowhead has an earlier alliance with Amgen Inc., signed in 2016.